Understanding The Different Types Of Property Coverage: A Comprehensive Guide

Understanding the Different Types of Property Coverage: A Comprehensive Guide

As a homeowner or business owner, one of the most important investments you can make is purchasing the right property insurance. With so many types of coverage available, it can be overwhelming to navigate the world of property insurance. In this article, we’ll break down the different types of property coverage, explaining what they cover, how they work, and which ones are right for you.

What is Property Coverage?

Property coverage is a type of insurance that protects your physical assets, such as your home, building, or personal belongings, against damage or loss. It’s designed to help you recover financially in the event of a disaster, theft, or other unexpected event. Property coverage can be purchased as a standalone policy or as part of a broader insurance package.

Types of Property Coverage

There are several types of property coverage, each with its own unique features and benefits. Here are some of the most common types of property coverage:

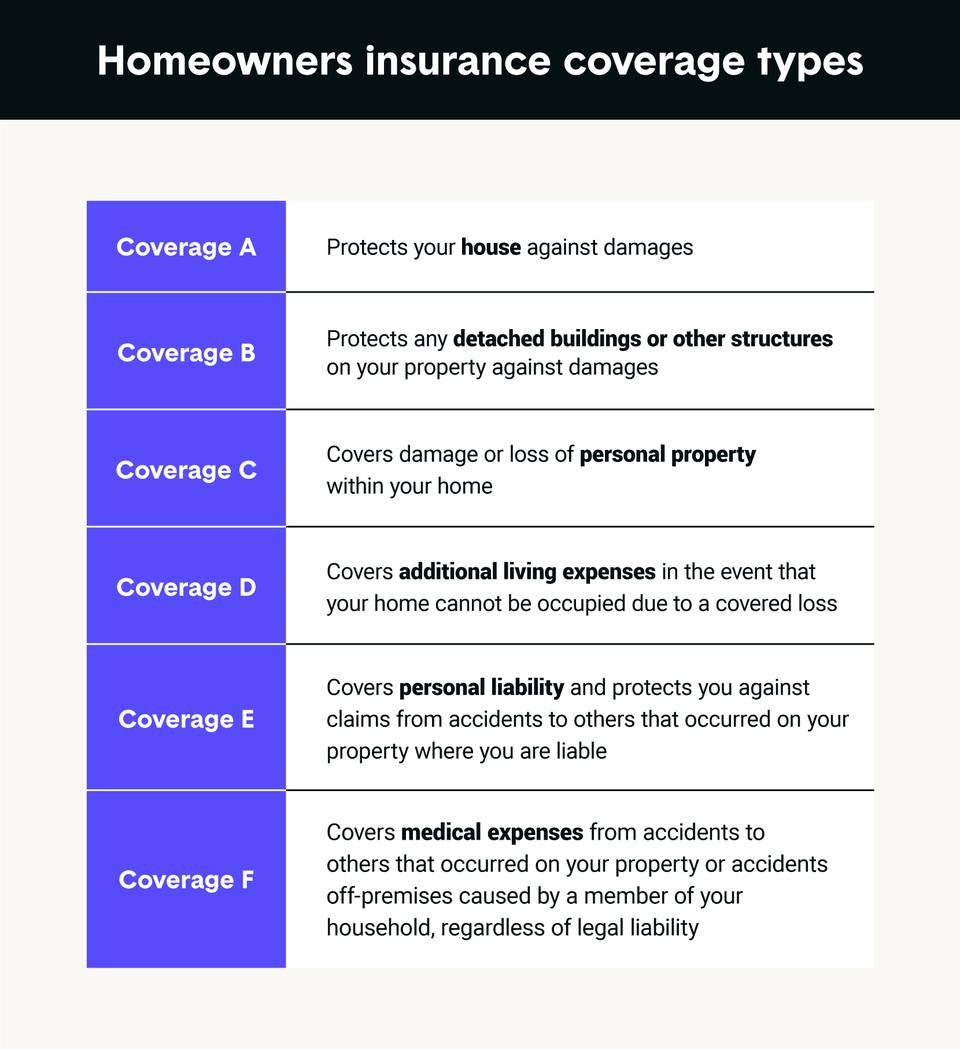

Dwelling Coverage: This type of coverage protects the physical structure of your home, including the walls, roof, and foundation. It’s typically included in a standard homeowners insurance policy. Dwelling coverage will help pay for repairs or rebuilding costs if your home is damaged or destroyed due to a covered event, such as a fire, tornado, or hurricane.

Personal Property Coverage: This type of coverage protects your personal belongings, such as furniture, electronics, and clothing. It’s also typically included in a standard homeowners insurance policy. Personal property coverage will help pay for replacement or repair costs if your belongings are damaged or stolen.

Liability Coverage: This type of coverage protects you in the event that someone is injured on your property. Liability coverage will help pay for medical expenses, lost wages, and other related costs. It’s also typically included in a standard homeowners insurance policy.

Flood Insurance: This type of coverage protects against damage caused by flooding. It’s typically purchased as a separate policy, as standard homeowners insurance policies usually don’t cover flood damage. Flood insurance is highly recommended for homeowners living in flood-prone areas.

Earthquake Insurance: This type of coverage protects against damage caused by earthquakes. It’s typically purchased as a separate policy, as standard homeowners insurance policies usually don’t cover earthquake damage. Earthquake insurance is highly recommended for homeowners living in earthquake-prone areas.

Renters Insurance: This type of coverage protects renters against damage to their personal belongings and liabilities in the event of an accident or disaster. Renters insurance is similar to homeowners insurance, but it only covers the renter’s personal belongings and liabilities.

Condo Insurance: This type of coverage protects condominium owners against damage to their unit and personal belongings. Condo insurance is similar to homeowners insurance, but it only covers the individual unit and not the entire building.

Mobile Home Insurance: This type of coverage protects mobile homeowners against damage to their home and personal belongings. Mobile home insurance is similar to homeowners insurance, but it’s specifically designed for mobile homes.

Landlord Insurance: This type of coverage protects landlords against damage to their rental properties and liabilities in the event of an accident or disaster. Landlord insurance is similar to homeowners insurance, but it’s specifically designed for rental properties.

Commercial Property Insurance: This type of coverage protects businesses against damage to their property and equipment. Commercial property insurance is highly customizable and can be tailored to meet the specific needs of your business.

How Does Property Coverage Work?

Property coverage works by providing financial protection against physical damage or loss to your assets. Here’s a step-by-step guide on how property coverage works:

- Purchase a policy: You purchase a property insurance policy that meets your needs and budget.

- Pay premiums: You pay premiums on a regular basis, either monthly or annually.

- File a claim: If your property is damaged or lost, you file a claim with your insurance company.

- Assessment: An adjuster will assess the damage to determine the extent of the loss.

- Payment: If the damage is covered under your policy, your insurance company will pay you the amount of the claim.

Tips for Choosing the Right Property Coverage

Choosing the right property coverage can be overwhelming, but here are some tips to help you make an informed decision:

- Assess your risks: Consider the risks associated with your property, such as natural disasters, theft, and accidents.

- Determine your coverage limits: Decide how much coverage you need based on the value of your assets.

- Choose the right deductible: Select a deductible that works for you, keeping in mind that a higher deductible means lower premiums.

- Consider multiple policies: If you have multiple properties or assets, consider purchasing multiple policies to ensure adequate coverage.

- Read reviews and compare policies: Research insurance companies and compare policies to find the best one for you.

Conclusion

Property coverage is an essential investment for anyone who owns or rents property. With so many types of coverage available, it’s essential to understand what each type covers and how it works. By choosing the right property coverage, you can protect your assets and finances in the event of unexpected events. Remember to assess your risks, determine your coverage limits, choose the right deductible, and consider multiple policies. With the right property coverage, you can have peace of mind knowing that you’re protected against life’s uncertainties.

Comments

Post a Comment