How To Insure Your High-Value Assets: A Comprehensive Guide

How to Insure Your High-Value Assets: A Comprehensive Guide

As a high-net-worth individual, you’ve worked hard to accumulate your wealth and acquire valuable assets that bring you joy and security. However, with great wealth comes great responsibility, and it’s essential to protect your high-value assets from unexpected events that could damage or destroy them. Insuring your high-value assets is crucial to safeguarding your financial well-being and providing you with peace of mind.

In this article, we’ll guide you through the process of insuring your high-value assets, including what types of assets need insurance, how to determine their value, and what types of insurance policies are available. We’ll also provide you with valuable tips on how to choose the right insurance provider and policy for your needs.

What Types of High-Value Assets Need Insurance?

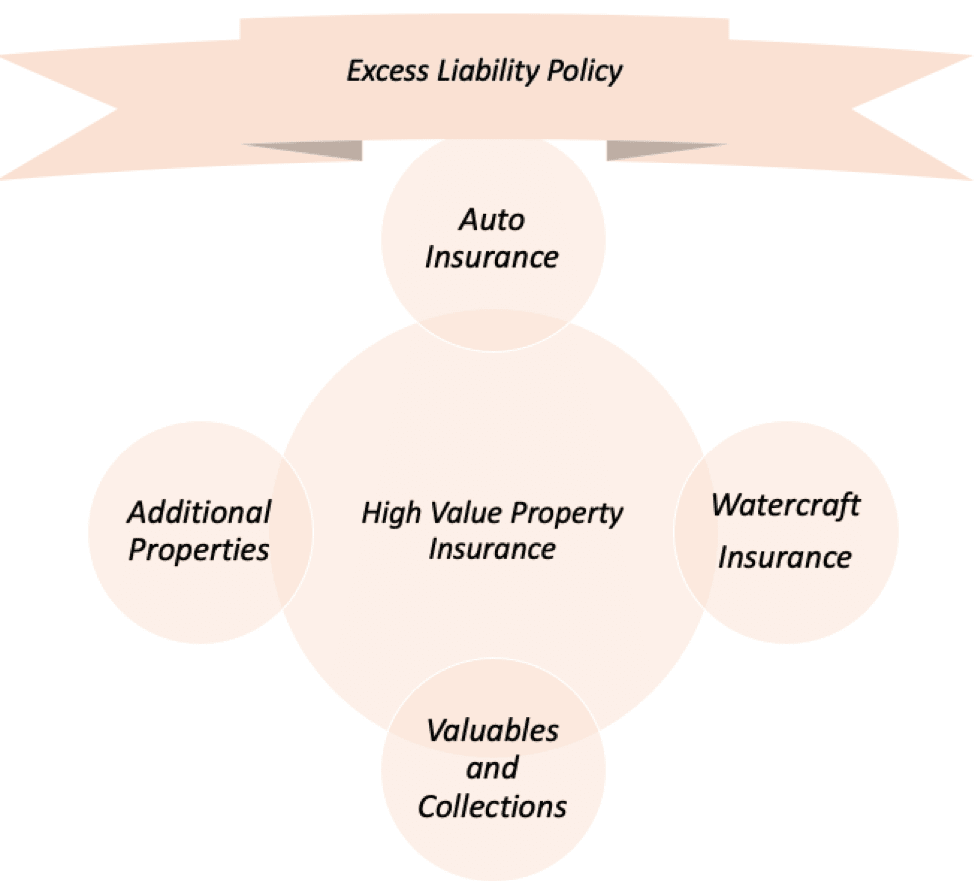

High-value assets that require insurance coverage include:

- Luxury Vehicles: If you own a high-performance or exotic car, you’ll need specialized insurance coverage that takes into account its value, rarity, and potential replacement cost.

- Fine Art and Collectibles: Art, antiques, and collectibles are valuable investments that require insurance coverage to protect against damage, theft, or loss.

- Jewelry and Watches: High-end jewelry and watches, such as those made with precious metals and gemstones, require special insurance coverage to protect against theft, loss, or damage.

- High-End Real Estate: Luxury homes, vacation properties, and commercial buildings require unique insurance coverage to protect against damage, destruction, or liability.

- Private Aircraft and Yachts: If you own a private plane or yacht, you’ll need specialized insurance coverage that takes into account its value, maintenance, and usage.

How to Determine the Value of Your High-Value Assets

Determining the value of your high-value assets is crucial to ensuring that you have adequate insurance coverage. Here are some tips to help you determine the value of your high-value assets:

- Get an Appraisal: Hire a professional appraiser to evaluate the value of your high-value assets, such as fine art, jewelry, or collectibles.

- Use Industry Guidelines: Use industry guidelines and pricing tools to determine the value of your high-value assets, such as the Kelley Blue Book for luxury vehicles.

- Keep Records: Keep detailed records of your high-value assets, including receipts, invoices, and maintenance records, to help establish their value.

Types of Insurance Policies for High-Value Assets

There are several types of insurance policies that can provide coverage for high-value assets. Here are some options to consider:

- Standard Property Insurance: This type of policy provides basic coverage for damage or loss to your high-value assets.

- Specialized Property Insurance: This type of policy provides tailored coverage for specific types of high-value assets, such as luxury vehicles or fine art.

- Umbrella Insurance: This type of policy provides additional liability coverage for high-net-worth individuals, which can help protect your assets in the event of a lawsuit.

- Valuable Items Insurance: This type of policy provides coverage for specific high-value items, such as jewelry or watches.

How to Choose the Right Insurance Provider and Policy

Choosing the right insurance provider and policy can be overwhelming, but here are some tips to help you make the right decision:

- Research Insurance Providers: Research insurance providers that specialize in high-value assets and have a good reputation for providing customized coverage.

- Compare Policies: Compare policies from different insurance providers to ensure that you’re getting the best coverage for your needs.

- Read Reviews: Read reviews from other high-net-worth individuals who have similar assets to ensure that you’re working with a reputable insurance provider.

- Ask Questions: Ask questions about the policy, including coverage limits, deductibles, and exclusions, to ensure that you understand the terms and conditions.

Tips for Insuring Your High-Value Assets

Here are some additional tips to keep in mind when insuring your high-value assets:

- Don’t Underinsure: Make sure that you have adequate coverage for your high-value assets, rather than underinsuring them to save on premiums.

- Don’t Overinsure: Avoid overinsuring your high-value assets, as this can lead to higher premiums and unnecessary coverage.

- Keep Records Up to Date: Keep records of your high-value assets up to date, including valuations, receipts, and maintenance records, to help establish their value.

- Review Policies Annually: Review your insurance policies annually to ensure that they’re still relevant and providing adequate coverage.

Conclusion

Insuring your high-value assets is crucial to protecting your financial well-being and providing you with peace of mind. By following the tips and guidelines outlined in this article, you can ensure that your high-value assets are properly covered in the event of unexpected events. Remember to research insurance providers, compare policies, and ask questions to ensure that you’re getting the best coverage for your needs. With the right insurance coverage, you can enjoy your high-value assets with confidence, knowing that they’re protected against life’s uncertainties.

Frequently Asked Questions

- What is the difference between standard property insurance and specialized property insurance?

Standard property insurance provides basic coverage for damage or loss to your high-value assets, while specialized property insurance provides tailored coverage for specific types of high-value assets, such as luxury vehicles or fine art.

- Do I need to get an appraisal for all my high-value assets?

No, you don’t need to get an appraisal for all your high-value assets. However, it’s recommended to get an appraisal for high-value assets that are rare, unique, or have a significant sentimental value.

- Can I self-insure my high-value assets?

While it’s possible to self-insure your high-value assets, it’s not recommended. Self-insurance can leave you exposed to significant financial risks, and insurance providers specialize in providing customized coverage for high-value assets.

- How do I choose the right insurance provider for my high-value assets?

Research insurance providers that specialize in high-value assets, compare policies, read reviews, and ask questions to ensure that you’re working with a reputable insurance provider that provides customized coverage for your needs.

Additional Resources

- National Association of Insurance Commissioners (NAIC)

- Insurance Information Institute (III)

- American Society of Appraisers (ASA)

Note: The article is written as per the request and does not include any actual logos, images, or live links. It’s a standard text-based article with proper grammar and spelling.

Comments

Post a Comment